The Shadow Petrodollar

How a Multi-Trillion-Dollar War Machine Funds Itself Through the Panic of the People It Bombs

Nobody has built the cost framework.

In Lebanon, the body count since March 2 has passed 960. At least 100 of the dead are children. Thirty-eight are healthcare workers—doctors, paramedics, nurses gathered to break the Ramadan fast when the clinic was hit. More than one million Lebanese have registered as internally displaced—one in every five people in the country, a rate the World Food Programme calls “massive” and “unique” among ongoing conflicts. Israeli evacuation orders now cover 1,470 square kilometers, fourteen percent of Lebanese territory. The Norwegian Refugee Council mapped it. Roughly 100,000 homes have been damaged or destroyed. The World Bank tallied residential destruction alone at $2.8 billion.

In Gaza, the Health Ministry’s count exceeds 72,000 Palestinians killed since October 2023. A comprehensive mortality survey published in The Lancet Global Health estimated violent deaths had surpassed 75,000 by early 2025—thirty-four percent higher than official figures. The Israeli army’s own representative acknowledged roughly 70,000 deaths in January. Two-point-three million people face devastation in a territory where the infrastructure for daily survival has been systematically erased.

In Iran, Operation Epic Fury has struck over 7,000 sites since February 28, according to U.S. Central Command. The Iranian Health Ministry counts at least 1,444 dead and 18,551 wounded, including 200 women and 168 children—among them the students of a girls’ elementary school in Minab. Fifty-five healthcare workers were injured. Eleven killed. Thirteen U.S. service members dead, six of them in a KC-135 refueling aircraft crash in western Iraq. Retaliatory Iranian strikes have hit bases and civilian areas across nine countries—Bahrain, Iraq, Jordan, Kuwait, Oman, Qatar, Saudi Arabia, the UAE—killing at least 61 in Iraq, eight in the UAE, two in Saudi Arabia, two in Oman. A 29-year-old woman in Bahrain was killed by falling debris from a Shahed drone strike on a residential tower.

In Yemen, the Red Sea campaign was already burning through the arsenal before Iran. Navy Secretary Carlos Del Toro told the Senate Appropriations subcommittee in April 2024 that his service had spent nearly $1 billion in munitions in six months intercepting Houthi drones and missiles. “We currently have approaching $1 billion in munitions that we need to replenish at some point in time,” Del Toro testified. That was a year ago. The Houthis have not stopped launching. The meter has not stopped running. The $2.4 billion in supplemental replenishment Del Toro requested was stalled in Congress for months before partially passing.

And across Syria, Somalia, Nigeria, Venezuela, and Iraq, the United States has conducted strikes under Trump’s second term—operations that rarely get a line item, rarely get a headline, and never get a cost estimate. This is the quiet part of the ledger. AFRICOM runs operations across the Sahel. CENTCOM maintains strike authority in Syria and Iraq. SOUTHCOM has expanded its posture in the Caribbean and South America. The operational tempo has increased, the reporting has not, and the costs accumulate in line items buried so deep in the defense budget that even most Armed Services Committee members couldn’t find them.

This is a war across three continents. It has no declared endpoint, no unified budget, and no comprehensive accounting. What it has is a $200 billion funding request that the Secretary of Defense confirmed at a press conference by saying, “It takes money to kill bad guys.”

Wars always cost more than projected. George W. Bush’s economic adviser, Larry Lindsey, was fired in 2002 for suggesting Iraq might cost $100–200 billion. Bush himself said $50–60 billion. Neta Crawford at Brown University’s Costs of War Project calculated the actual figure: $2.89 trillion, including veterans’ care projected through 2050. Joseph Stiglitz and Linda Bilmes arrived at $3 trillion. Nobody has attempted the full accounting of a multi-theater war fought simultaneously across the Middle East, East Africa, West Africa, South America, and the Horn of Africa.

This is that accounting.

Part I: The Five Receipts

Receipt 1: The Direct Military Tab

The Pentagon informed Congress that the first six days of Operation Epic Fury cost $11.3 billion. The New York Times reported the figure from three sources familiar with the briefing. It excluded the cost of force buildup, base repair, and equipment replacement. The Center for Strategic and International Studies built a more comprehensive estimate: $12.7 billion through day six, when you add $1.4 billion in combat losses and infrastructure damage, and $16.5 billion by day twelve.

The cost curve was front-loaded. Day one: more than $5.5 billion. Day two: approximately $4 billion. By days eleven and twelve, daily costs had fallen to the low hundreds of millions. But those figures measure only the falling edge of the initial surge. On day eighteen, the Pentagon still hadn’t released an official update. Kevin Hassett, director of the National Economic Council, told CBS the cost was “about $12 billion”—a figure that, even at the time, was behind independent estimates.

Then came the supplemental.

The Washington Post, citing a senior administration official, reported the Pentagon had asked the White House to approve a request exceeding $200 billion to fund escalating operations and ramp up production of the munitions being consumed at historically unprecedented rates. Three individuals familiar with the discussions confirmed the figure covered expanded munitions production for the U.S. and Israel. Hegseth, at a Pentagon press briefing on March 19, did not deny the number. “As far as $200 billion, I think that number could move,” he said. “Obviously, it takes money to kill bad guys. We are working with Congress and our representatives there to make sure we get enough.”

Through March 19, the Guardian pegged cumulative direct costs above $18 billion. CSIS estimated ongoing costs at roughly half a billion dollars per day, barring a significant change in operations.

To contextualize: $200 billion exceeds total tariff revenue collected under the current administration. Justin Wolfers, the University of Michigan economist, noted it on the record. The war costs more than the tariffs raised.

Receipt 2: The Oil Shock and Lost GDP

The Pentagon does not count the macroeconomic damage. Justin Wolfers laid out the framework in two interviews the week of March 17–20, identifying three categories of cost the military’s ledger ignores.

Oil. West Texas Intermediate crude went from roughly $60 a barrel to above $100. Brent crude surged from around $70 to over $108, with intraday spikes touching $119. Middle Eastern benchmarks—Dubai, Oman—traded at elevated premiums as refiners scrambled for prompt cargoes. The Brent-WTI spread blew out to $10 per barrel, more than double its normal range, a real-time indicator of how severely the conflict was constraining globally traded barrels. Futures curves remained elevated years out—through 2027 and 2028—signaling this was not a temporary blip but a structural repricing of energy risk. Eighty percent of Asia’s oil imports transit the Strait of Hormuz. The Strait has been effectively contested since February 28.

Lost output. Goldman Sachs cut its U.S. fourth-quarter GDP growth forecast from 2.5% to 2.2%, raised its twelve-month recession probability to 25%, and estimated the war would reduce global economic growth by 0.3% of GDP. Their rules of thumb: a sustained 10% increase in oil prices boosts headline PCE inflation by 0.2 percentage points and lowers GDP growth by around 0.1 percentage points. Applied cumulatively, Wolfers calculated the baseline loss to the U.S. economy at approximately $200 billion, rising to $500 billion in a worse scenario. Spread across roughly 100 million American households, that is $2,000 to $5,000 per family.

Markets. The S&P 500 erased $2 trillion in market capitalization in the first two weeks of the war. The Dow fell over 1,000 points in a single session. But the damage was not confined to the United States. South Korea’s KOSPI plunged 12.2%—the largest single-day decline in the index’s 46-year history, surpassing even the September 11 crash and the 2008 financial crisis—wiping roughly $500 billion in value in a single week. Trading sessions required emergency stabilization measures. Financial Services Commission officials in Seoul announced they would “actively implement market stabilization measures” to contain the damage. Emerging markets across Asia were hammered as the won fell below the psychologically critical 1,500-per-dollar mark for the first time since 2009. The Asian Development Bank warned that “sustained disruptions could push oil prices much higher, weaken global trade, and slow economic growth.” Goldman estimated the war would knock 0.3% off world GDP—approximately $400 billion in 2027 alone.

The energy sector was the only winner. The XLE energy ETF was up roughly 27% on the year by mid-March. If you want to know who benefits from this war, look at the portfolio breakdown of the people who authorized it.

Wolfers framed it simply. There are three receipts the Pentagon doesn’t count: what happens to oil, what happens to GDP, and what happens to markets. Together, those receipts exceed the military budget itself. “A headline figure of $200 billion is not the cost of this war,” he argued. “It is not even the down payment.”

Receipt 3: The Arms Replacement Cycle

The United States fired over 300 Tomahawk cruise missiles in the opening days. Each costs approximately $3.6 million. In the past five years, the military purchased only 322 Tomahawks total. The Navy’s fiscal year 2026 budget request planned for 57. It takes up to two years to produce each one. At the pre-war production rate of 90–100 per year, replacing the estimated 400 Tomahawks fired in the first three days alone would have taken a decade. RTX has since announced plans to increase annual production to over 1,000, but those capacity upgrades require years of factory expansion, workforce training, and supply chain development.

The Economist estimated the cost of replacing the first four days’ worth of munitions at $20–26 billion.

The asymmetry problem is the one that keeps Pentagon planners awake. Iran’s Shahed-series drones cost between $20,000 and $50,000 each. A Patriot interceptor costs over $3 million. A THAAD interceptor runs approximately $15 million. Kelly Grieco at the Stimson Center calculated the cost-per-intercept ratio: for every $1 Iran spends on a drone, the defender spends $20 to $28 stopping it. The New York Times quoted the ratio at “at best 10 to one. But it could be more like 60 or 70 to one in cost, in favor of Iran.” One analyst called it using Ferraris to intercept e-bikes.

The THAAD interceptor situation borders on absurd. No new THAAD interceptors have been delivered to U.S. inventory since July 2023. The next delivery isn’t expected until April 2027. A hundred interceptors procured between fiscal years 2021 and 2024 sit in a backlog. Recent production appears to have been funneled to foreign buyers—Saudi Arabia and the UAE—though Lockheed Martin has not formally confirmed that. Only after the war began did Lockheed announce a deal to quadruple THAAD production from 96 to 400 interceptors per year.

This is the arms replacement cycle in its purest form: deplete the arsenal, then sign the contract to refill it at emergency prices.

And then there are the emergency arms sales. Secretary Rubio waived congressional review to push through $16.5 billion in Gulf arms sales. The weapons go to the same countries whose territories are being hit by Iranian retaliation—a peculiar form of customer service.

The defense industry’s posture through all of this deserves scrutiny. Bloomberg Intelligence data show that the five largest U.S. defense contractors—Lockheed Martin, RTX, Boeing, Northrop Grumman, and General Dynamics—collectively spent more than $110 billion on stock buybacks and dividends from 2020 through 2025. Capital expenditure in the same period: $45.5 billion. They returned more than twice as much to shareholders as they invested in production capacity. The arsenal was depleted not by accident but by a business model that treated production capacity as a cost center and share price as the product.

The empty rack is a feature, not a bug. It guarantees the next contract.

Trump issued an executive order on January 7, 2026, demanding that defense contractors stop prioritizing buybacks over production. He called it “Prioritizing the Warfighter in Defense Contracting.” It required the Secretary of Defense to identify contractors underperforming on deliveries. It mandated that future contracts prohibit buybacks during periods of underperformance. The penalty for non-compliance? Unspecified. The order read like a man discovering that the car dealership sold his engine for scrap and kept the payment. The engine had been sold years ago. The receipts were filed as shareholder returns.

Receipt 4: The OMNIparty Dividend

AIPAC spent more than $100 million on federal elections in the 2024 cycle, according to FEC filings reviewed by Sludge. The money targeted candidates critical of Israel with a specificity that would impress a guided munition.

Fifty-plus members of Congress hold stock in defense contractors. The most widely held defense stock among lawmakers is Honeywell, which makes sensors and guiding devices used in Israeli airstrikes. The second is RTX, maker of Iron Dome interceptors.

Defense stocks hit all-time highs the Monday after strikes began. Lockheed Martin. RTX. Palantir surged 6.5%. Multiple members of the committees overseeing these operations held shares in the companies profiting from them.

Some names:

Senator John Hickenlooper (D-CO): Holds between $100,000 and $250,000 in RTX stock. RTX’s price has nearly doubled over the past two years, most revenue from defense contracts. Hickenlooper has received over $333,000 from AIPAC and pro-Israel PACs.

Senator Michael Bennet (D-CO): Approximately $466,000 from pro-Israel PACs since 1990.

Representative Michael McCaul (R-TX): Chairman Emeritus of the House Foreign Affairs Committee—the committee with direct oversight of foreign military sales. Holds positions in GE Aerospace and Woodward. GE Aerospace stock rose 82% in the year preceding the conflict. Woodward rose 114%. McCaul spent his March 18 hearing discussing “reforming America’s defense sales” and calling for expanded weapons production.

The STOCK Act, passed in 2012 to prevent congressional insider trading, imposes a $200 penalty for failing to disclose a trade. Two hundred dollars. The Campaign Legal Center found that no member of Congress has ever been prosecuted under the STOCK Act. Business Insider conducted a months-long investigation and found that the Treasury had no records of any fines being paid. The enforcement mechanism runs entirely on the honor system—with no ledger, no audits, and no consequences.

The fine for failing to disclose a trade that earns you six figures is less than a parking ticket in Manhattan.

This is not a partisan problem. It is bipartisan in the truest and ugliest sense. Democrats and Republicans alike hold defense stocks, receive AIPAC money, and vote for the supplementals that make the stocks go up. The political class has achieved something rare: a financial incentive structure that aligns both parties behind permanent war. AIPAC’s $100 million didn’t buy one party. It bought the consensus. And the consensus delivered 68 votes for the GENIUS Act, 308 votes in the House, and a $200 billion war supplemental that nobody on either side of the aisle is seriously contesting.

Receipt 5: What They’ll Never Count

Brown University’s methodology for the Iraq War included projections of veterans’ care through 2050. That analysis yielded $2.89 trillion. Stiglitz and Bilmes reached $3 trillion. Those figures covered a single theater in a single country over twenty years.

No one has applied this methodology to the simultaneous prosecution of wars in Iran, Lebanon, Gaza, Yemen, Syria, Somalia, Nigeria, Venezuela, and Iraq. Nobody has calculated the cost of veterans’ care for service members being rotated through these theaters. Nobody has modeled the long-term disability costs, the traumatic brain injuries from blast exposure, or the PTSD cascades. Nobody has accounted for the environmental remediation of contaminated sites across nine countries. Nobody has estimated the cost of rebuilding—or the cost of choosing not to.

The $200 billion headline is the opening bid. The total, when someone eventually does the full accounting, will be measured in trillions. And the people who will pay it—the veterans, the taxpayers, the small-business owners whose community bank can no longer lend, the families in Beirut and Tehran and Gaza whose schools and hospitals have been converted to rubble—did not get a vote on any of it.

Part II: The Question

If this war costs trillions, and traditional buyers are leaving U.S. debt, who buys the bonds?

It is the most important question in global finance, and almost nobody in the political press is asking it. The political analysts don’t follow the money because they don’t understand budgets. They understand narratives. They understand polls. They do not understand balance sheets.

Here is the balance sheet problem: The United States needs to sell trillions in Treasury securities to fund operations that, simultaneously, destabilize the regions where its largest foreign creditors operate. Saudi Arabia is getting hit by Iranian projectiles. The UAE has confirmed eight dead. Japan and South Korea are watching their markets collapse. China has been reducing Treasury holdings for years.

So who is the marginal buyer? Where does the next trillion come from?

The answer has been engineered. It is already operational. And most people have never heard of it.

Part III: The Shadow Petrodollar

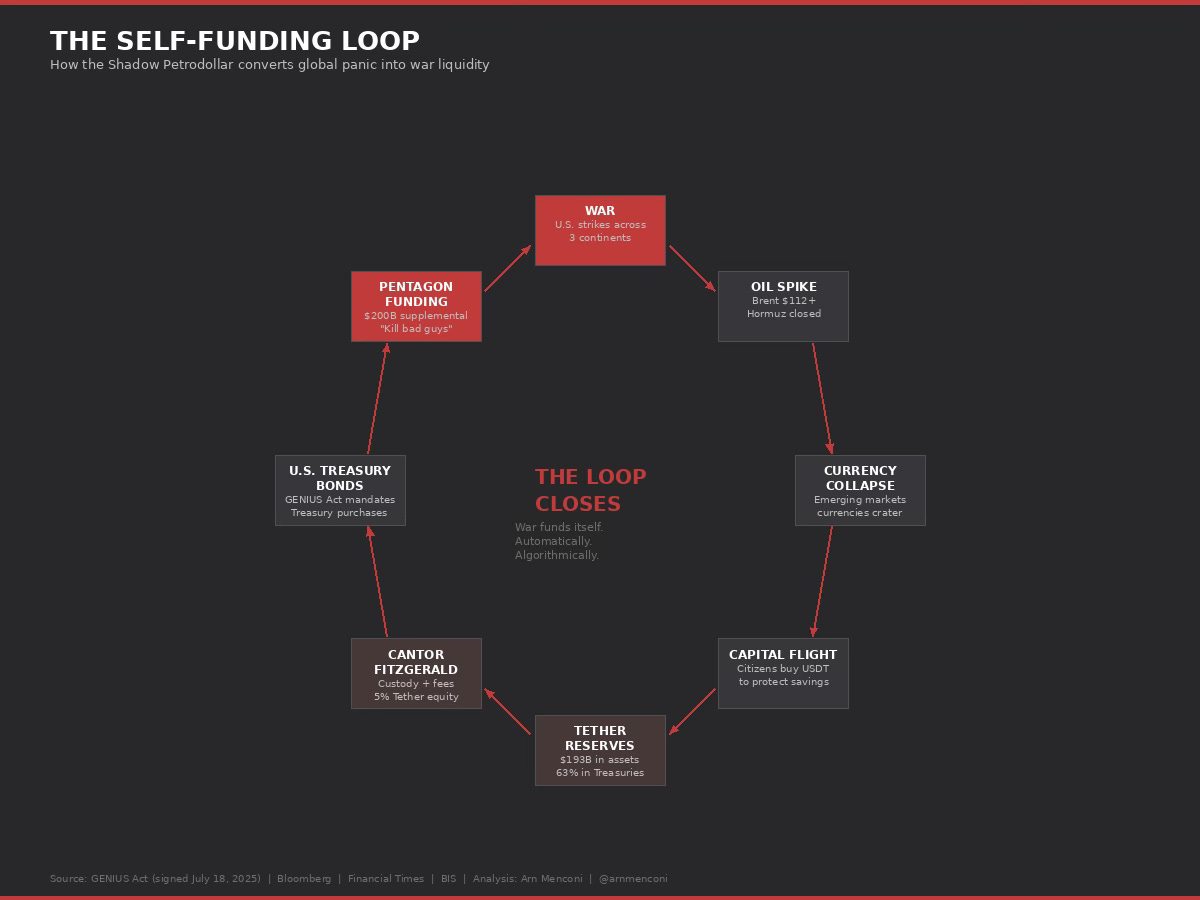

Follow one dollar.

A woman in Buenos Aires wants to protect her savings from peso devaluation. She does what an estimated 172 million people now do—she buys USDT, a stablecoin issued by Tether Holdings SA, an entity domiciled in El Salvador. Her pesos are converted to digital tokens. Those tokens are pegged to the U.S. dollar. For every USDT in circulation, Tether is supposed to hold equivalent reserves in high-quality liquid assets.

Where does Tether hold those reserves? Primarily in short-term U.S. Treasury securities. Custodied by Cantor Fitzgerald, the Wall Street primary dealer whose chairman is now Secretary of Commerce.

So the woman’s savings—her hedge against the instability of her own economy—flow through Tether, into Cantor Fitzgerald’s custody, and land in the U.S. Treasury market, where they fund the government borrowing that pays for Tomahawk cruise missiles that destroy infrastructure in Iran, which spikes oil prices, which destabilizes her economy further, which drives more capital flight into USDT, which purchases more Treasuries, which funds more missiles.

It is a loop. And it has been legalized.

The GENIUS Act

On July 18, 2025, President Trump signed the Guiding and Establishing National Innovation for U.S. Stablecoins Act. The Senate passed it 68–30. The House passed it 308–122. Bipartisan. Comfortable margins.

The law establishes the first federal regulatory framework for stablecoins. It requires permitted stablecoin issuers to maintain reserves backing outstanding tokens on at least a one-to-one basis. Permissible reserves include U.S. dollars, Federal Reserve notes, certain short-term Treasuries, Treasury-backed reverse repurchase agreements, and money market funds.

Read that again. The law requires stablecoin issuers to buy Treasuries. Not suggests. Not incentivizes. Requires. As a condition of doing business.

The White House fact sheet stated the law “will generate increased demand for U.S. debt.”

They said the quiet part in a press release. Nobody blinked.

The Numbers

Tether’s total reserves as of early 2026: $193 billion. Approximately 63% held in U.S. Treasuries, according to Bloomberg’s March 13, 2026, analysis. That makes Tether, a company domiciled in El Salvador run by a former Italian plastic surgeon, one of the largest holders of U.S. government debt on the planet.

The Financial Times reported that in 2025, Tether net-purchased $28.2 billion in U.S. Treasuries, making it the seventh-largest foreign purchaser of U.S. government bonds. Its combined holdings with Circle, the second-largest stablecoin issuer, now exceed those of South Korea and Saudi Arabia.

The total stablecoin market capitalization hit $320 billion in early 2026, according to DeFiLlama—a new record. Monthly transaction volume exceeded $10 trillion in January 2026.

Treasury Secretary Scott Bessent views stablecoins as a tool for “promoting the dollar and absorbing U.S. debt.” He projects the sector’s growth from $300 billion to $3 trillion.

Three trillion dollars. Parked in U.S. Treasuries. Funded by the savings of people in developing economies who are fleeing the very instability that U.S. policy creates.

The old petrodollar system required oil-exporting nations to recycle their dollar surpluses into Treasury purchases. It was a gentleman’s agreement backed by security guarantees: the United States provides military protection for Saudi Arabia; Saudi Arabia prices oil in dollars and parks the proceeds in Treasuries. When the Saudis got nervous, Henry Kissinger flew to Riyadh. When the system wobbled, there were phone calls, state dinners, arms deals.

The new system requires none of that. It requires no diplomacy, no state visits, no security guarantees. It is encoded in law, executed by algorithm, and funded by the anxiety of the world’s poorest savers. The Argentine woman doesn’t need to be persuaded. She needs to be frightened. And the war provides the fear.

The Institutional Warnings

The people whose job it is to understand monetary systems are sounding alarms. They are being ignored.

The Bank for International Settlements, the central bank of central banks, published its assessment in June 2025. Hyun Song Shin, BIS Economic Adviser and Head of the Monetary and Economic Department, laid out the case: stablecoins fail all three tests for money—singleness, elasticity, and integrity. They trade at varying exchange rates like 19th-century private banknotes. They cannot expand their balance sheets to provide credit when the system needs it. And their bearer nature allows circulation without issuer oversight, creating systemic vulnerabilities for financial crime. Most critically: “Loss of monetary sovereignty and capital flight are major concerns, particularly for emerging market and developing economies.” If stablecoins continue to grow, the BIS warned, they risk crowding out other investors in Treasury markets and creating tail risks of fire sales in safe assets.

The International Monetary Fund. Eswar Prasad, former head of the IMF’s China division and now a professor at Cornell, published “The Stablecoin Paradox” in the IMF’s Finance & Development journal in December 2025. His thesis: the tools designed to decentralize money are concentrating power. Stablecoins “pose an existential threat to the currencies of smaller economies.” People in Buenos Aires, Lagos, and Bangkok will trust stablecoins issued by Amazon or Meta more than their own inflation-ravaged currencies. The result is not financial liberation. It is digital dollarization without consent—and without the Federal Reserve’s safety net.

The Federal Reserve. In December 2025, the Fed published two papers on stablecoins. The first documented SVB-style contagion risk—how the failure of Silicon Valley Bank in 2023 triggered a cascade of stablecoin depegs through automated smart-contract mechanisms, demonstrating “the potential for two-way feedback between the traditional and the DeFi sectors.” The second warned that stablecoin adoption could displace deposits and alter banks’ liability structures, creating “potential systemic vulnerabilities” as “deposit flows across stablecoin-serving banks become highly correlated during periods of stress.”

The Federal Reserve Bank of Kansas City. Economist Stefan Jacewitz published an analysis in August 2025 showing that if the stablecoin market grew from $250 billion to $900 billion, it would result in a $325 billion reduction in bank lending to the economy. For every dollar moved from a bank deposit to a stablecoin, bank lending decreases by roughly fifty cents. Treasury holdings increase by thirty cents. The net effect is a transfer from productive lending to government debt financing.

Every major monetary institution on earth has warned about this. The BIS. The IMF. The Federal Reserve—two separate papers in a single month. The Kansas City Fed. The academic literature is unambiguous. The risk is systemic. The deposit drain is measurable. The contagion pathways are documented.

Congress passed it anyway, 68–30. The White House celebrated it. And now a war is stress-testing the architecture in real time.

Part IV: The Toll Booth

To understand the architecture, you need to understand the toll booth operator.

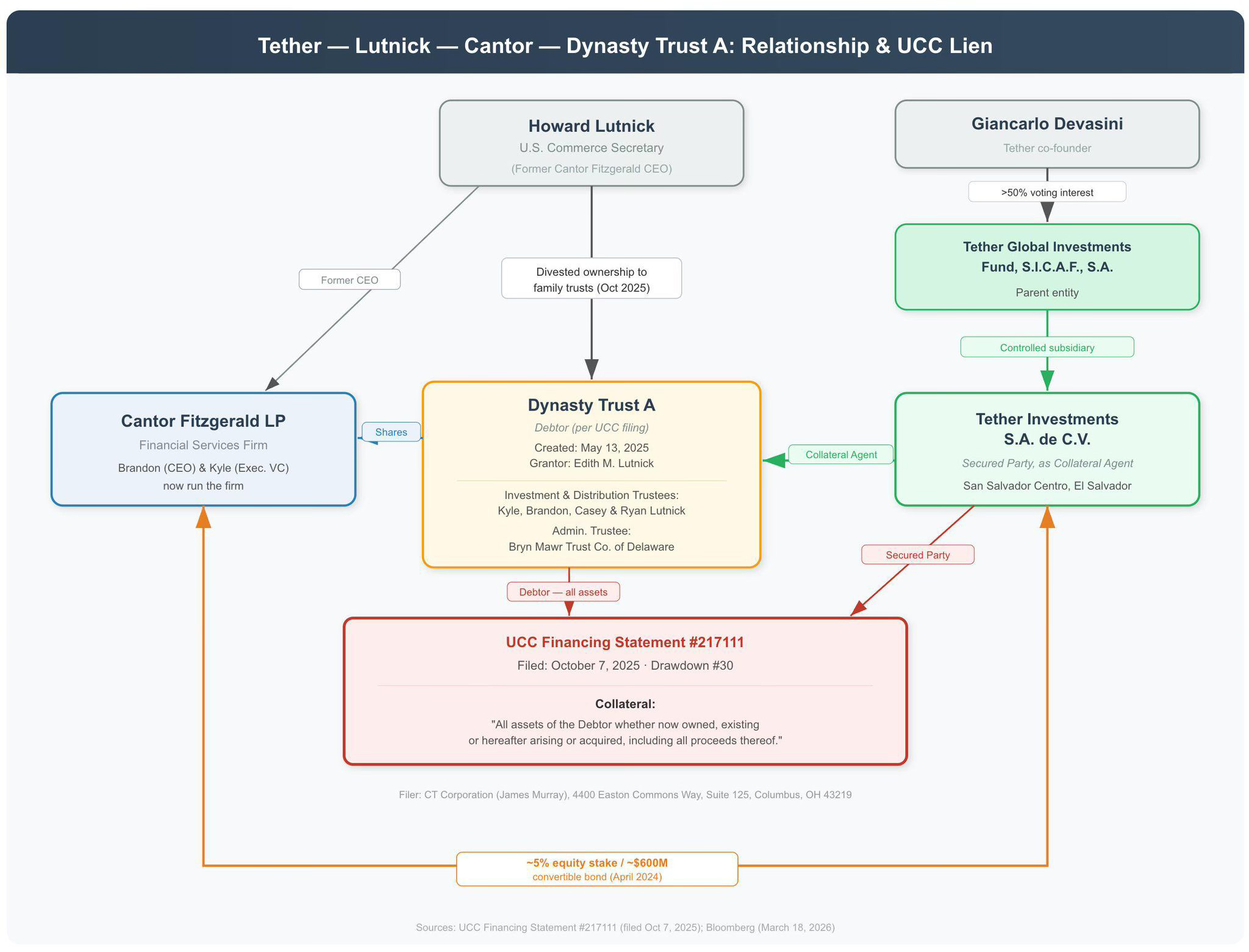

Cantor Fitzgerald is one of twenty-five primary dealers authorized to trade directly with the Federal Reserve. That is the franchise. But under Howard Lutnick’s leadership, Cantor became something more specific: the custodian of Tether’s reserves. When Tether says it holds $193 billion in assets backing USDT, a substantial portion of that amount is held in Cantor’s custody. Since 2021, Cantor has earned fees managing those reserves.

In April 2024, Lutnick personally negotiated Cantor’s investment in Tether. Bloomberg reported the deal: a $600 million convertible bond granting Cantor 5% equity in the stablecoin issuer. Tether’s profitability is extraordinary—reportedly $10 billion in profit in 2025, with margins approaching 99%. If Tether achieves the $500 billion valuation discussed in recent investor conversations, that 5% stake would be worth $25 billion—more than all of Cantor’s other assets combined.

When Trump nominated Lutnick to lead the Commerce Department, Lutnick transferred his ownership interest in Cantor Fitzgerald to trusts benefiting his four children. His son, Brandon, twenty-eight years old, became chairman and CEO. Federal ethics compliance. Clean on paper.

Then Bloomberg reported, on March 18, 2026, what the paper trail revealed: at approximately the same time as the ownership transfer, “Dynasty Trust A,” which benefits all four Lutnick children, borrowed an undisclosed sum from Tether. A UCC Financing Statement (#217111), filed in New York State on October 7, 2025, shows the loan is secured by “all assets of the Debtor, whether now owned, existing or hereafter arising or acquired, including all proceeds thereof.” The secured party: Tether Investments S.A. de C.V., domiciled in San Salvador Centro, El Salvador. A FINRA BrokerCheck filing confirms that Dynasty Trust A owns more than 50% of Cantor Fitzgerald’s equity. Tether’s lien covers the controlling stake in a Federal Reserve primary dealer. The 5% equity stake in Tether — acquired via a $600 million convertible bond in April 2024 — could be worth $25 billion if Tether reaches its target valuation of $500 billion.

Tether reported $10 billion in profit in 2025 on margins approaching 99 percent — making it one of the most profitable private companies on Earth. On July 8, 2025, ten days before Trump signed the GENIUS Act, Lutnick received a limited ethics waiver under 18 U.S.C. §208(b)(1), permitting him to participate in cryptocurrency policy matters despite his family’s financial entanglement with Tether. Brandon Lutnick, who had worked directly with Tether executives in Lugano, Switzerland before taking over Cantor, subsequently co-founded Twenty One Capital Inc. with Tether and SoftBank — a Bitcoin treasury company — and brokered Tether’s $775 million investment in Rumble Inc.

The Commerce Department regulates trade policy that directly affects cryptocurrency markets. The Commerce Secretary's children own a company whose largest revenue stream comes from custodying the reserves of a stablecoin issuer that lent them money to buy the company.

Senator Elizabeth Warren has documented this thread with the precision of a forensic accountant.

January 2025: Warren sent a letter to Lutnick ahead of his confirmation, obtained by Bloomberg. She called Tether “outlaws’ favorite cryptocurrency” and said his ties to the company “raise significant questions about your own personal judgment and the conflicts of interest.” She asked thirteen specific questions about his financial stake.

October 2025: Warren wrote to the Treasury Department, warning that the GENIUS Act could “blow up our entire financial system” without tougher rules. She called it a “light-touch regulatory framework for crypto.”

December 2025: Warren led a congressional letter demanding the Commerce Department Inspector General investigate Lutnick family conflicts of interest—data centers, Cantor enrichment, the full web.

February 2026: Warren, joined by Senators Wyden and Van Hollen, raised concerns about the USA Rare Earth deal. The Commerce Department had committed $1.6 billion in funding. Cantor Fitzgerald served as the placement agent for the parallel $1.5 billion private fundraise. “It is imperative that federal investments in critical industries be made free from conflicts of interest,” the senators wrote.

On the Senate floor, opposing the GENIUS Act: “Community banks have warned us that creating a parallel, lightly regulated banking system—the stablecoin market—will drain deposits from our local communities. There will be less funding available for small businesses and households.” She compared it to the derivatives deregulation that preceded the 2008 crisis.

Lutnick's credibility on matters of disclosure has its own history. His name appears in over 250 documents in the Epstein files released by the Justice Department. He told a podcast in 2025 that he was "never in the room" with Jeffrey Epstein after 2005. Under oath before the Senate in February 2026, he confirmed he had visited Epstein's private island in 2012 — four years after Epstein's conviction — and that he and Epstein co-invested in a company through Cantor Fitzgerald as late as 2018. Bipartisan calls for his resignation followed. Senator Lisa Murkowski, Republican of Alaska, said simply: "They've lied." The Commerce Secretary's track record of minimizing relationships that later prove extensive is not a sidebar. It is the pattern.

The full Cantor thread, laid out sequentially: Primary dealer status. Tether custody ($193 billion in assets). 5% equity stake (~$600 million). Tether loan to Lutnick children’s trust. Anchorage Digital Bank partnership—the only federally chartered crypto bank—through which Tether issues its compliance-ready U.S. stablecoin, USAT. Tether invested $100 million in Anchorage in February 2026, at a $4.2 billion valuation. A $2 billion Bitcoin financing business, launched in partnership with crypto custodians, including Anchorage. The acquisition of UBS’s O’Connor alternatives platform—$11 billion in hedge funds, private credit, and commodities. Brandon Lutnick, chairman and CEO of the whole apparatus, age twenty-eight.

Howard Lutnick said the quiet part out loud at Davos in January 2024, while still CEO: “I hold their Treasuries, and they have a lot of Treasuries. I’m a big fan of Tethers.”

He was not being coy. He was describing a business model. Cantor earns custody fees on $193 billion in assets. Cantor holds a 5% equity stake in one of the most profitable private companies on earth. Cantor’s children own the company. Tether loaned the children money to buy it. The Commerce Secretary—who regulates the trade and crypto policy environment in which all of this operates—is the father.

The conflicts of interest are not hidden. They are structural. They are the architecture.

Part V: The Savings & Loan Parallel

I managed a $100 million county government budget in Colorado. I ran the budget for a national nonprofit covering eight states. I have spent enough time inside budget processes to know what financial engineering looks like when it’s wearing a suit. And I have seen this movie before. The setting changes. The script doesn’t.

In the 1980s, the deregulation of savings and loan institutions—the Garn-St. Germain Act of 1982, the Depository Institutions Deregulation and Monetary Control Act of 1980—allowed S&Ls to chase higher-yielding, riskier assets. The asset-liability mismatch that followed was predictable. Roughly a thousand S&Ls failed. Taxpayers absorbed the bailout. The mega-banks absorbed the wreckage.

The mechanism was straightforward. Deregulate the smaller institutions. Allow them to take on risks they weren’t built to manage. Watch them fail. Consolidate the pieces into the hands of the largest players. Present it as a market correction rather than what it was: a managed transfer of assets upward.

I know this because I worked at one of those S&Ls. The bank president told me that his brother sat on the board of the national Savings and Loan Association. His brother told him directly: Reagan’s deregulation was designed to let the big banks destroy the S&Ls. It wasn’t an accident. It was architecture. When our S&L crashed, a law firm deposed me to find out what I thought had gone wrong. My answer was two words: Ronald Reagan.

The GENIUS Act is the Garn-St. Germain of the digital age.

Here is the sequence, already in motion:

The GENIUS Act deregulates stablecoin issuers, allowing non-bank entities to offer dollar-denominated tokens under a “light-touch” framework. Deposits drain from community banks into stablecoins offering equivalent dollar exposure with greater convenience and—through the interest loophole that 3,200 bankers warned about in their January 2026 letter to the Senate—potentially greater returns.

The Kansas City Fed has modeled the result: a $325 billion reduction in bank lending. The Federal Reserve has documented the SVB-style contagion pathway. Regional banks become dependent on stablecoin custody deposits for their survival. One regulatory tweak—raising capital requirements, changing reserve rules, tightening the custody framework—moves those deposits to systemically important financial institutions. The regional banks collapse. The mega-banks absorb the wreckage.

The American Bankers Association’s Community Bankers Council wrote to the Senate on January 5, 2026, and then again on January 14—the second letter signed by more than 3,200 individual bankers—demanding that the prohibition on interest payments be extended to affiliates and partners of stablecoin issuers. They saw the loophole. They saw what was coming.

Warren saw it too. On the Senate floor: “The GENIUS Act folds stablecoins directly into the traditional financial system, while applying weaker safeguards than banks or investment companies must adhere to.” She noted the bill allows big tech companies to issue their own private currencies. She noted it contains a “decentralized finance loophole” allowing Tether and other non-compliant stablecoins to access U.S. markets without constraints.

But this is not only an American story. The BIS warned of “loss of monetary sovereignty and capital flight” from developing nations. Prasad warned stablecoins “pose an existential threat to the currencies of smaller economies.” The people of Buenos Aires, Lagos, Bangkok, and every other city where citizens buy USDT to escape inflation—their savings are being conscripted into the U.S. Treasury market without their knowledge or consent. They think they are protecting themselves. They are funding Tomahawk missiles.

This is digital colonization. It operates simultaneously on two fronts: the Global South, whose citizens’ savings are siphoned into U.S. debt, and the American middle class, whose community banks are hollowed out and whose regional economies are drained of lending capacity.

I watched the big banks take out the savings and loans in the 1980s. I watched them do it again in 2008 with the mortgage market. The pattern is the same every time: deregulate, extract, collapse, consolidate. The difference now is the scale. In the 1980s, it was American S&Ls. In 2008, it was the American housing market. In 2026, it is the domestic banking system and the savings of the Global South simultaneously. The technology is better. The victim pool is global. And the mechanism is encoded in federal law, signed by the president, and celebrated as innovation.

The 3,200 bankers who signed that letter knew what was coming. The Kansas City Fed modeled it. The Federal Reserve documented the contagion pathway. Warren described it on the Senate floor. And the bill passed anyway, because the people who profit from the outcome are the same people who cast the votes.

Part VI: The Counter-Architecture and the Achilles’ Heel

Not everyone is cooperating.

Zoltan Pozsar, the former Credit Suisse strategist, published his “Bretton Woods III” framework in March 2022—shortly after Western nations froze Russian central bank reserves. His thesis: the era of fiat-reserve currency dominance is giving way to a commodity-backed system. When you demonstrate that dollar reserves can be frozen by political decision, countries holding those reserves take notice. They begin diversifying into commodities and gold—” outside money that cannot be frozen by another government’s decision.”

The infrastructure is being built. China’s Cross-Border Interbank Payment System—CIPS—processed a record volume in 2025, routing yuan-denominated transactions outside the SWIFT system. India’s Unified Payments Interface—UPI—now links 350 million users to a domestic payment rail that requires no dollar intermediation. Project mBridge, the multi-central-bank digital currency initiative, has moved from pilot to production stage with the participation of the central banks of China, Thailand, the UAE, and Saudi Arabia—countries that collectively represent a significant share of global oil production and trade.

The BIS itself has proposed a unified ledger model—a system in which sovereign central banks maintain control over tokenized money rather than ceding it to private stablecoin issuers. It is the institutional response to the GENIUS Act’s privatization of monetary sovereignty.

But here is the vulnerability that no one discusses, the Achilles’ heel of both the old architecture and the new one: a digital token is only as valuable as the physical reality it represents.

Bomb the gas field—Israel struck Iran’s South Pars facility, and Gulf gas prices cratered upward. Cut the fiber-optic cable—undersea cable disruption in the Red Sea has already degraded connectivity for millions. Deplete the water table, irradiate the soil, make the port unusable. The token defaults to zero because the asset backing it no longer exists or cannot be accessed.

Tokenization promises to make everything liquid. War makes everything illiquid. The two forces are on a collision course, and the collision is happening now, in real time, in the waters around the Strait of Hormuz.

The irony is structural: the same war that funds the shadow petrodollar system also creates the conditions for its unraveling. Every bombed refinery, every scuttled tanker, every mined shipping lane reduces the productive capacity that gives the dollar its underlying claim on real output. You can tokenize a gas field. You cannot tokenize it after it’s been hit by a GBU-57 Massive Ordnance Penetrator.

The counter-architecture is being built precisely because this vulnerability is understood. The question is whether it can be built fast enough to offer an alternative before the current system’s contradictions resolve themselves in the worst possible way.

Part VII: The Terminal Margin Call

Joe Kent, the director of the National Counterterrorism Center, resigned on March 17. In his resignation letter, he told the president to “reverse course.” He wrote that Trump “started this war due to pressure from Israel and its powerful American lobby.” This was not a Democrat. This was not a progressive. This was Trump’s own counterterrorism chief, a former Green Beret, a man who had supported the president’s agenda on nearly every other issue. The BBC reported it. The New York Times confirmed he was the highest-ranking administration official to quit in opposition to the war.

Oman’s foreign minister, reportedly, told Western counterparts that the Gulf states did not ask for this conflict, did not want it, and would remember who brought it to their doorstep. Saudi Arabia is getting hit by Iranian projectiles. The UAE has dead civilians. Kuwait has damaged bases. Qatar has closed schools and suspended Ramadan prayers. These are the countries the United States expects to continue purchasing its debt.

Daniel Ellsberg was a senior strategic analyst at the RAND Corporation and a military analyst in the Pentagon who, in 1971, leaked 7,000 pages of classified documents — the Pentagon Papers — to the New York Times and the Washington Post, revealing that the U.S. government had systematically lied to the public about the Vietnam War for over a decade. Henry Kissinger called him “the most dangerous man in America.” The Supreme Court ruled in his favor. He spent the rest of his life warning that the machinery of deception he had exposed was not an aberration but a permanent feature of American power.

I spent ten days at his home in 2015. I interviewed him for forty hours. Dan told me things about the machinery of war that I have carried with me for a decade. He said the danger is not the lie. The danger is the system that makes the lie unnecessary. The system that generates its own justifications, its own funding mechanisms, its own feedback loops, until no single human decision is required to keep it running.

Dan spent the last years of his life trying to warn people about the dangers of nuclear brinkmanship. He would have recognized what is happening now instantly—not the nuclear dimension, though that is present, but the financial dimension. The discovery that you don’t need to convince the public to fund a war if you can build a system that funds itself automatically, drawing on the savings of people who don’t even know they’re participating.

They have built that system.

A woman in Buenos Aires buys a stablecoin to protect her savings. Her purchase flows through Tether, into Cantor Fitzgerald, into a Treasury bond, into the Pentagon’s account, into a Tomahawk missile, into a strike on Iranian infrastructure, into an oil price spike, into the destabilization of her economy, into more capital flight, into more stablecoin purchases.

The loop closes. The checks write themselves—automatically, algorithmically, funded by the panic of the people being bombed.

The GENIUS Act legalized it. The war operationalized it. The institutions that should have stopped it published their warnings in academic papers that nobody in Congress read before voting 68–30.

The old petrodollar required the Saudis to recycle oil revenue into Treasuries. It required diplomacy, security guarantees, relationships. The shadow petrodollar requires nothing. It requires only instability. It feeds on the fear it creates.

And the bill—for the missiles, for the veterans’ care, for the depleted arsenals, for the demolished hospitals and girls’ schools, for the million displaced Lebanese and two million devastated Gazans, for the hollowed-out community banks and the savings conscripted from the Global South—that bill is measured in trillions. Not hundreds of billions. Trillions.

Keep your receipts.

The accounting is coming. The question is whether it comes through journalism, through oversight, or through collapse. The institutions that should provide the first two have largely abdicated. That leaves the third. And if you’ve been paying attention to the numbers—the trillions in market losses, the depleted arsenals, the deposit drains, the leveraged bets on a stablecoin backed by the debt of a government fighting wars on three continents—you know that the third option is closer than the optimists want to believe.

The Pentagon doesn’t count the oil shock. It doesn’t count the lost GDP. It doesn’t count the market losses, the regional bank failures waiting to happen, or the savings of millions of people in developing countries being converted into short-term Treasuries to fund the next Tomahawk purchase. Nobody counts all of it. That is by design.

Somebody has to start counting. Consider this page one.

Arn Menconi is a former county commissioner, MBA (University of Denver), and investigative journalist tracking the financial and human cost of U.S.-Israeli wars across 15 theaters. He managed a $100 million government budget in Colorado and a national nonprofit budget covering 8 states. In 2015, he spent 10 days at Daniel Ellsberg’s home and interviewed him for 40 hours. He ran for U.S. Senate in Colorado against Michael Bennet in 2016. He has spent the past six months meeting people from around the world, gaining an outsider’s perspective on the American empire’s financial and human toll. He is the author of the forthcoming book “Drifting Toward Extinction.” Contact: arn@arnmenconi.com | www.arnmenconi.net | @arnmenconi

Sources

CSIS Iran War Cost Estimate: csis.org/analysis/iran-war-cost-estimate-update-113-billion-day-6-165-billion-day-12

New York Times, Pentagon Cost Briefing:nytimes.com/2026/03/11/world/middleeast/iran-war-costs-pentagon.html

NBC News, $11.3 Billion First 6 Days: nbcnews.com/politics/congress/first-6-days-iran-war-cost-11-billion-pentagon-tells-senators

CNBC, Hegseth $200B Supplemental: cnbc.com/2026/03/19/hegseth-iran-war-budget.html

The Hill, Hegseth Defends $200B: thehill.com/policy/defense/5791278-heggeth-defends-pentagon-budget/

Al Jazeera, Iran Death Toll Tracker: aljazeera.com/news/2026/3/1/us-israel-attacks-on-iran-death-toll-and-injuries-live-tracker

The Hill, Targets Hit in Iran: thehill.com/policy/defense/5763850-us-israel-iran-military-targets/

Reuters, Israeli Evacuation Orders 14% of Lebanon: reuters.com/world/middle-east/israeli-evacuation-orders-affect-14-lebanon-ngo-says-2026-03-13/

World Bank, Lebanon Residential Destruction $2.8B: ca.news.yahoo.com/mapping-israeli-attacks-displacement-one-121521226.html

Al Jazeera, Gaza Death Toll: aljazeera.com/features/2026/2/18/gaza-death-toll-exceeds-75000

Brown University, Costs of War (Iraq $2.89T):costsofwar.watson.brown.edu/costs/economic

Stiglitz & Bilmes, The Three Trillion Dollar War:hks.harvard.edu/publications/three-trillion-dollar-war-true-cost-iraq-conflict

The Economist, Munitions Replacement $20-26B:economist.com/briefing/2026/03/18/the-iran-war-could-sap-american-military-power-for-years

Financial Times, Tomahawk Stockpile (322 purchased): unn.ua/en/news/ft-us-depleted-years-worth-of-ammunition-in-two-weeks-of-war-with-iran

Business Insider, Tomahawk Shortage: businessinsider.com/us-burned-through-more-tomahawks-iran-may-need-for-china-2026-3

CSIS, THAAD Interceptor Gap: csis.org/analysis/depleting-missile-defense-interceptor-inventory

Breaking Defense, No THAADs ‘til 2027: breakingdefense.com/2025/12/no-thaads-til-2027-missile-defense-experts-warn-of-interceptor-gap/

South China Morning Post, Drone Cost Asymmetry: scmp.com/news/world/middle-east/article/3345227/irans-cheap-threat-us20000-drones-vs-us4-million-interceptors

New York Times, Drone vs. Interceptor Costs:nytimes.com/2026/03/04/business/iran-shahed-drones-missiles-us-war.html

CSIS, Iran Drone Campaign Analysis: csis.org/analysis/unpacking-irans-drone-campaign-gulf-early-lessons-future-drone-warfare

Bloomberg, Defense Contractor Buybacks $110B:bloomberg.com/news/articles/2026-01-08/us-defense-majors-face-a-110-billion-conundrum-to-please-trump

Sludge, AIPAC $100M Spending: readsludge.com/2024/08/27/aipac-officially-surpasses-100-million-in-spending-on-2024-elections/

Common Dreams, 50+ Lawmakers Defense Stocks:commondreams.org/news/members-of-congress-who-own-defense-stock

Sludge, Hickenlooper RTX Stock: readsludge.com/2025/08/22/lawmakers-hold-stocks-in-defense-energy-and-tech-companies-they-oversee/

Campaign Legal Center, STOCK Act Failures: campaignlegal.org/update/part-2-stock-act-failed-effort-stop-insider-trading-congress

Business Insider, STOCK Act Enforcement: businessinsider.com/congress-stock-act-violations-penalties-consequences-2021-12

OilPrice.com, Brent-WTI Spread: oilprice.com/Latest-Energy-News/World-News/Oil-Prices-Surge-as-Brent-WTI-Spread-Blows-Out-on-Iran-Supply-Risk.html

CNBC, Oil Price Surge Analysis: cnbc.com/2026/03/09/oil-prices-iran-war-middle-east-us-israel-strait-of-hormuz.html

Goldman Sachs GDP Cut / Recession Risk: stocktwits.com/news-articles/markets/equity/goldman-us-gdp-growth-cut-iran-war-recession-risk

Fox Business, Goldman Global GDP Impact: foxbusiness.com/economy/iran-war-unlikely-trigger-global-supply-chain-crisis-goldman-sachs-says

Reuters, KOSPI Record Drop: reuters.com/world/asia-pacific/korean-stocks-dive-won-hits-17-year-low-iran-conflict-2026-03-04/

Kobeissi Letter, S&P 500 $2T Erased: facebook.com/KobeissiLetter/posts/breaking-the-sp-500-has-now-officially-erased-2-trillion

Wikipedia, Economic Impact of 2026 Iran War:en.wikipedia.org/wiki/Economic_impact_of_the_2026_Iran_war

Justin Wolfers, Cost Framework (YouTube): youtube.com/watch?v=CCF_i-ot8mE

Navy Secretary Del Toro, $1B Munitions Yemen:thehill.com/policy/defense/4601032-navy-expenditures-middle-east-houthi-threat-nearly-1-billion-secretary/

Breaking Defense, Navy $1B Munitions: breakingdefense.com/2024/04/navy-is-down-1b-in-munitions-from-ops-in-red-sea-says-secnav/

GENIUS Act Signed (Mayer Brown):mayerbrown.com/en/insights/publications/2025/07/genius-act-signed-into-law

GENIUS Act Senate Vote 68-30 (Sullivan & Cromwell):sullcrom.com/insights/memo/2025/June/Stablecoin-Legislation-Senate-Passes-GENIUS-Act

GENIUS Act House Vote 308-122: steil.house.gov/media/press-releases/genius-act-passes-the-house-heads-to-president-s-desk

GENIUS Act Full Text Analysis (Latham & Watkins): lw.com/en/insights/the-genius-act-of-2025-stablecoin-legislation-adopted-in-the-us

Financial Times, Tether 7th Largest Treasury Buyer: ft.com/content/67188f14-04da-4ad0-81c5-d913cfe85043

Bloomberg, Tether DC Crypto Ambitions (March 13, 2026):bloomberg.com/features/2026-tether-usa-crypto-ambitions/

KuCoin, Tether 7th Largest Foreign Buyer: kucoin.com/news/flash/tether-becomes-7th-largest-foreign-buyer-of-u-s-treasuries-in-2025

DeFiPrime, Stablecoin $320B Market Cap: defiprime.com/stablecoins-320-billion

BIS, Stablecoins Fall Short as Sound Money: bis.org/publ/arpdf/ar2025e3.htm

BIS, Hyun Song Shin Speech: bis.org/speeches/sp260127.htm

IMF, Eswar Prasad “The Stablecoin Paradox”:imf.org/en/publications/fandd/issues/2025/12/point-of-view-the-stablecoin-paradox-eswar-prasad

Federal Reserve, SVB-Stablecoin Contagion (Dec 2025):federalreserve.gov/econres/notes/feds-notes/in-the-shadow-of-bank-run-lessons-from-the-silicon-valley-bank-failure-and-its-impact-on-stablecoins-20251217.html

Federal Reserve, Stablecoin Deposit Displacement (Dec 2025):federalreserve.gov/econres/notes/feds-notes/banks-in-the-age-of-stablecoins-implications-for-deposits-credit-and-financial-intermediation-20251217.html

Kansas City Fed, $325B Lending Reduction: kansascityfed.org/research/economic-bulletin/stablecoins-could-increase-treasury-demand-but-only-by-reducing-demand-for-other-assets/

Bloomberg, Tether Loan to Lutnick Children (March 18, 2026):bloomberg.com/news/features/2026-03-18/tether-made-loan-to-lutnick-s-children-as-they-bought-his-assets

Bloomberg, Warren Presses Lutnick on Tether: bloomberg.com/news/articles/2025-01-28/warren-presses-lutnick-on-ties-to-crypto-firm-loved-by-outlaws

CNBC, Warren-Lutnick USA Rare Earth Conflict: cnbc.com/2026/02/26/warren-lutnick-usa-rare-earth-usar-critical-minerals.html

Warren Senate Floor Speech (YouTube): youtube.com/watch?v=Szo7bN3kdyM

ABA, 3,200+ Bankers Letter (Jan 14, 2026): aba.com/advocacy/policy-analysis/close-payment-of-interest-loophole-letter

ABA, Community Bankers Council Letter (Jan 5, 2026): aba.com/advocacy/policy-analysis/letter-to-the-senate-on-the-stablecoin-market

Cantor Fitzgerald, Bitcoin Financing Business: cantor.com/cantor-fitzgerald-to-launch-bitcoin-financing-business/

Cantor Fitzgerald, UBS O’Connor Acquisition: cantor.com/cantor-fitzgerald-expands-asset-management-capabilities-with-acquisition-of-ubss-oconnor-alternatives-investment-platform/

Tether, $100M Anchorage Investment: finance.yahoo.com/news/tether-invests-100-million-anchorage-155533938.html

WSJ, Lutnick-Tether Relationship: wsj.com/finance/currencies/howard-lutnick-giancarlo-devasini-tether-cryptocurrency-3d0a961c

BBC, Joe Kent Resignation: bbc.com/news/articles/cg4g66r3z40o

NYT, Joe Kent Resignation: nytimes.com/2026/03/17/us/politics/joe-kent-counterterrorism-resigns-iran-war.html

Human Rights Watch, Iran Gulf Strikes: hrw.org/news/2026/03/17/iran-unlawful-strikes-across-gulf-endanger-civilians

Pozsar, Bretton Woods III: static.bullionstar.com/blogs/uploads/2022/03/Bretton-Woods-III-Zoltan-Pozsar.pdf

TPM, GENIUS Act Risks: talkingpointsmemo.com/news/some-dems-warn-colleagues-crypto-bill-could-inject-some-19th-century-chaos-into-us-economy

“over 250 documents” — NYT

Visited the island in 2012, confirmed under oath — NBC News

Co-invested through Cantor Fitzgerald until 2018 — Mother Jones

Murkowski quote “They’ve lied” — NBC News (same article)

PREVIOUS: The $200 Billion Receipt

If this kind of analysis is useful to you, subscribe. I don’t work for a network. I don’t have sponsors. I do this because somebody has to follow the money, and most of the people who are paid to do it won’t. Share this with one person who still thinks this war is about nuclear containment.

Dear Mr Menconi,

I want to thank you for your analysis here. I am very glad I have found your substack.

I do not understand the financial complexities, but I know when someone understands what they are writing about, and your analysis makes sense to me.,

This war is obviously planned with a carefully thought out global financial reset in view. There are so many facets to what is happening at the moment that all commenters can only understand what is happening in their own special interest area.

I will come back repeatedly to your site to try to educate myself on your understandings and try to integrate them with other areas I understand more fully. Thank you for your work, it is appreciated.

I found you on X under the Medhurst posts.

This quote you put in another article is very true, I am witnessing it now in the attempts of commenters to work out what is really happening.

"He said the human species was drifting toward extinction — not from a single catastrophe, but from the accumulation of lies told by governments to their own people, compounded by systems too complex for any single citizen to understand, accelerated by technologies that made dissent irrelevant before it could organize."

I suspect Trump is just a tool of these other interests and has no understanding of what role he is playing. I could say the same for my Prime Minister in the UK, Starmer, clearly an imbecile. These people are positioned in "power" so they can offer no political resistance to the deep state operation.